I’m a restorative dentist who got a hard wake-up call during the 2008 financial crisis. Since then, I’ve poured thousands of hours into understanding money, risk, and why costs keep rising in healthcare. I share the most useful, actionable resources I’ve found—especially for dentists, but helpful to anyone—so you can protect your financial health and your practice. That’s why I built The Bitcoin Dental Network. It’s free, practical, and no strings attached.

Serious 2008 déjà vu

|

Hello Reader, Many of you have already heard about the “baptism by fire” Jean and I experienced in 2008 after borrowing a cool $1 million to build out our brand-new dental suite. I won’t bore you again with the details other than to say this week’s Article of the Week has my hair standing on end and a serious sense of déjà vu. Thinking through the parallels between today and what was unfolding in 2007 is enough to elevate my heart rate a bit. The good news is that this article also outlines prudent, actionable steps all of us can consider taking. And before anyone asks: no, I do not have any financial relationship with James Lavish. This piece was curated the old-fashioned way: because I think it’s important and worth your time. Without further introduction, here is this week’s Article of the Week. 💡 Is Private Credit a Black Swan in Plain View?Issue 209James Lavish, CFAMar 15, 2026∙ Paid ✌️ Welcome to the latest issue of The Informationist, the newsletter that makes you smarter in just a few minutes each week. 🙌 The Informationist takes one current event or complicated concept and simplifies it for you in bullet points and easy to understand text. 🫶 If this email was forwarded to you, then you have awesome friends, click below to join! 👉 And you can always check out the archives to read more of The Informationist. Today’s Bullets:

Inspirational Tweet:

If you’re a normal everyday person, you probably don’t think about private credit too often, if at all. And why should you? That’s for your pension fund or 401(k) manager to worry about. Until this last week. Because you’ve probably noticed that it’s been all over the news, seemingly everywhere you turn. If the article is not about war, it’s about private credit. But what exactly is private credit? Why is everyone talking about it all of a sudden? Why should you care? And most importantly, how could it possibly affect your own investments? All good questions and ones that we will answer, nice and easy as always, here today. So pour yourself a big cup of coffee and settle into your favorite seat for a look inside the private credit market with this Sunday’s Informationist. Partner spot.Most People Will Waste This Cycle

Bitcoin bear markets test your wits—and create opportunity for those prepared to act. Our new field guide, 21 Moves to Make in the Downturn, walks you through a clear, practical plan to steady your thinking, accumulate with discipline, and strengthen your long-term position while others lose focus. Inside, you’ll learn:

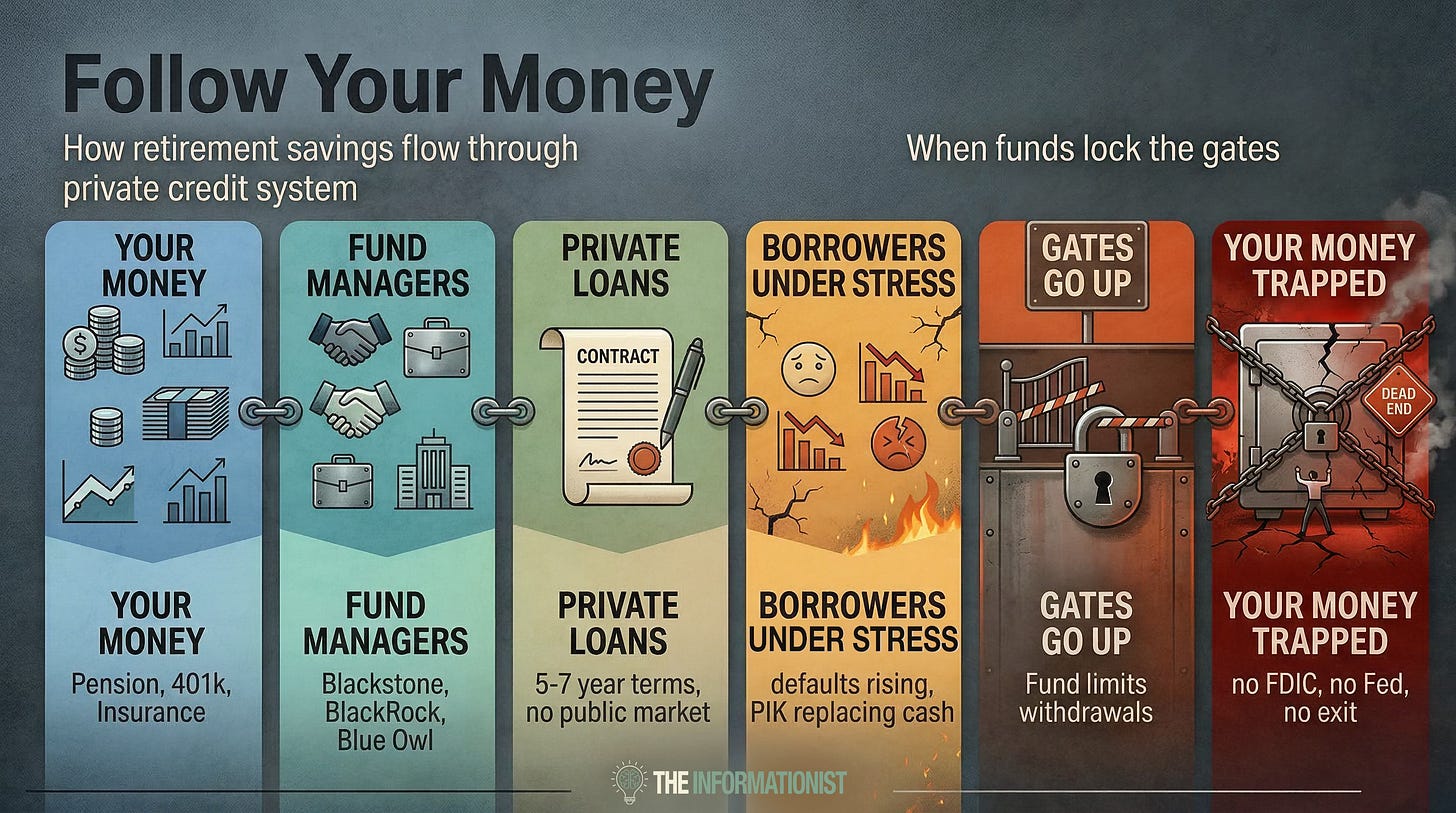

A small minority will quietly make the moves that matter. We wrote 21 Moves to Make in the Downturn for that minority. If you’re serious about building a position that survives the next decade, start here. 🏦What Is Private Credit, and Why Should You Care?Let’s start with the basics, shall we? You’ve probably heard of private equity. Big firms like KKR and Apollo that buy entire companies, restructure them, and sell them for a profit. That’s private equity, a sector of investing with its own can of mark-to-market worms. Private credit is different. It’s the lending side. See, instead of buying companies, private credit funds lend money to them. Think of it as unregulated banks, operating in the opaque corners of the bankng world, and making loans directly to mid-sized businesses that can’t or don’t want to borrow from traditional banks. This is why they’re often referred to as shadow banking. It’s lending outside of the traditional banking system, beyond the reach of most banking regulations. So why does private credit even exist? Simple. After super restrictive bank rules were enacted in the aftermath of the great financial crisis, fund managers saw an opportunity. They raised money from investors, from pensions, endowments, insurance companies, and wealthy individuals, and started making the loans that banks no longer would. Higher interest rates. Flexible terms. And for the investors putting money in, attractive yields in a world where yields were close to zero. Everybody won. The companies got their capital. The investors got their returns. The fund managers collected their fees. And the market grew like black mold in a Houston basement. FYI, I wrote all about shadow banking last fall. If you have not seen that newsletter or would like to revisit, you can find it here:

James Lavish, CFA·September 14, 2025Read full story Today, including committed capital and leverage, the global market has ballooned to roughly $3 trillion | 41,966,846 BTC. Larger than the entire global high-yield bond market. Now here’s who’s actually in this market because this is where it gets personal. Your pension fund is almost certainly allocated to private credit. If your 401(k) has an “alternative income” option, there’s a good chance it includes private credit. Life insurance companies are some of the biggest buyers. University endowments, too. You may never have heard the words “private credit” before today. But your retirement money has. OK so far so good, right? Companies get loans. Investors get yield. What could go wrong? Well, a lot of these funds were originally built with long lockup periods. You put your money in, it’s tied up for seven to ten years. The fund makes loans, collects interest, and when the loans mature, it returns your capital. The timelines match. Money goes in long. Money comes out long. Makes sense. But over the past few years, Wall Street got creative. They built a new kind of private credit fund. Perpetual funds. Evergreen funds. Names that sound like they’ll last forever. And in a way, that’s the problem. These funds have short lockups, sometimes just a year, sometimes none at all. After that, investors can request redemptions every quarter. There’s usually a cap, around 5% of the fund’s total value per quarter. Sounds reasonable, right? Here’s the catch. The loans inside these funds still last five to seven years. But unlike traditional funds, perpetual funds never stop lending. When an old loan gets repaid, the manager doesn’t hold that cash for redemptions. He recycles it into a brand new loan. More yield. More fees. The wheel never stops spinning. So now you have a fund full of five-to-seven-year loans that keeps making new five-to-seven-year loans, while promising investors they can leave every quarter through a 5% exit door. When only a few people head for the door each quarter, the math works. The fund keeps enough cash on hand. Nobody notices. But what happens when 7% want out? Or 9%? Or 14%? The fund can’t call up its borrowers and say, “We need that $50 million | 699 BTC back by Friday.” Those loans are locked. The cash isn’t there. It’s been recycled into new loans that won’t mature for years. So the fund has two choices. Sell the loans at fire sale prices. Or shut the door. It’s called putting up the gates.

When I wrote about private credit last fall, I flagged this structural mismatch. I said defaults could hit 5% if rates stayed high. They did. But I also said contagion was unlikely. I am now concerned about that last part. Because over the past few weeks, the gates have started closing. And the names on the doors are unfortunately ones you know. But the gates aren’t even the part that should worry you. 💣 The Dominoes That Started FallingIt started quietly. On February 18th, a fund called Blue Owl Capital did something unusual. They permanently halted redemptions on their $1.6 billion | 22,382 BTC credit fund, OBDC II. No more quarterly windows. No more exit door. They called it “ratable liquidity,” a fancy way of saying they’d return money on their own schedule. The market shrugged. Blue Owl isn’t exactly a household name. And $1.6 billion | 22,382 BTC, while not nothing, isn’t the kind of number that moves headlines. But inside the industry, people noticed. Because Blue Owl didn’t just limit redemptions. They eliminated them. Two weeks later, Blackstone reported numbers on BCRED, their $82 billion | 1,147,094 BTC flagship private credit fund. The biggest in the world. Investors had requested 7.9% of the fund back in a single quarter. Record redemptions. Nearly $6.5 billion | 90,928 BTC worth of “please give me my money back.” Blackstone honored the requests. But to do it, they wrote a check for $400 million | 5,596 BTC out of their own pocket. The largest alternative asset manager on the planet, backstopping its own fund with its own cash. And they still called it “noise.” Then came BlackRock. On March 7th, the world’s largest asset manager announced it was capping withdrawals on its $26 billion | 363,713 BTC private credit fund. Investors had requested 9.3% of the fund. BlackRock said no. Five percent was the maximum. The rest would have to wait. When BlackRock puts up the gates, people pay attention. Next up: Cliffwater. One of the biggest sellers of private credit to everyday retail investors. Their $33 billion | 461,635 BTC fund saw 14% redemption requests. They capped it at 7%. If you asked for a million back, you got five hundred thousand. The rest stays in the fund. Remember, this is the same Cliffwater whose fund has reported only three negative months of performance since it launched in 2019. Through COVID. Through the rate shock. Through the banking crisis. Three down months in nearly seven years. We’ll come back to that number. It matters more than you think. And then, just as I write this mid-week, Morgan Stanley capped redemptions on their North Haven Private Income Fund at 5%. That one wasn’t even on anyone’s radar two days ago. Five firms. Three weeks. Blue Owl. Blackstone. BlackRock. Cliffwater. Morgan Stanley. And here’s the one that made Mohamed El-Erian sit up and take notice. JPMorgan, the largest bank in the United States, started marking down software-linked loans to these very funds. And reducing new lending to them. Why does software matter? Because around 40% of private credit loans are concentrated in the software and enterprise technology sector. The same sector that AI is currently hollowing out. UBS warned last month that private credit defaults could hit 15% in a worst case. No recession, but rather a structural disruption of the borrower base. When JPMorgan marks down your loans, well, as the old E.F. Hutton commercial used to say... Everyone listens. But Jamie Dimon’s words were even more alarming: “I probably shouldn’t say this, but when you see one cockroach, there are probably more. And so we should, everyone should be forewarned on this one.” We just found five in three weeks. And the bank that’s best at finding cockroaches is the one pulling back.

This is the chain. Your money goes into a fund. The fund makes loans. When borrowers can’t pay, the fund locks the gates. And when the banks that lend to the funds start pulling back, the oxygen gets cut off entirely. It happened in 2007 when BNP Paribas froze three funds. Eighteen months later, Lehman collapsed. El-Erian made that exact comparison last week. And he’s not someone who throws around 2008 references lightly. The dominoes are alarming. The math behind them is worse. 🔍 Why the Numbers Don’t Add UpNow look, gating is not automatically a red flag. We just walked through the structural mismatch. When a wave of redemptions hits a fund full of long-duration loans, putting up the gates is responsible management. It prevents fire sales that would hurt everyone who stays. So I’m not going to tell you that gating alone means the sky is falling. But I want you to think about something. Remember Silicon Valley Bank? I wrote all about it at the time. If you haven’t read that issue or want to revisit, you can find the article here:

James Lavish, CFA·March 12, 2023Read full story For today’s purposes, though, SVB held a massive portfolio of long-duration US Treasuries and mortgage-backed securities. Safe assets. Government-backed. The kind of thing that’s supposed to be bulletproof. SVB was allowed to carry those bonds at full value under something called held-to-maturity accounting. The CFA Institute later called it “Hide-’Til-Maturity” accounting. Here’s what was hiding. $15.1 billion | 211,233 BTC in unrealized losses against $16.3 billion | 228,020 BTC in total equity. The losses alone would have wiped out 93% of the bank’s equity. On paper, SVB looked fine. In reality, it was a zombie. Then in March 2023, SVB tried to sell $21 billion | 293,768 BTC worth of bonds to raise cash. They took a $1.8 billion | 25,180 BTC loss. And the moment sophisticated depositors saw that number, they did the math on the rest of the portfolio. Forty-two billion dollars walked out the door in a single day, and 48 hours later, the bank was closed. *poof* But the bonds weren’t legally mis-marked. The accounting rules just allowed a gap between what the books said and what reality looked like. And when investors figured out the size of that gap, they stampeded toward the exit. Now think about private credit. These funds don’t hold Treasuries. They hold private loans to mid-sized companies. Loans that don’t trade on any exchange. Loans with no visible market price. Now you may be asking, how do the funds value them, then? And true to their Wall Street investment banking training, they build models, of course. Their own models. With their own assumptions. And here’s where it gets a bit slippery. They report those valuations to investors as if they’re fact. It’s called mark-to-model. And it’s the private credit version of “Hide-’Til-Maturity.” At least with SVB, you could look up the market price of a Treasury bond and do the math yourself. The fair value was buried in the footnotes, but it was there. With private credit, there are no footnotes. There’s no public market to check against. You’re trusting the fund manager’s model. You’re trusting the student to grade his own homework. First, Blue Owl reported their loan portfolio at 99.7 cents on the dollar. Practically perfect. Then they permanently halted redemptions. Huh. I mean, if your loans are really worth 99.7 cents, you sell a few at 97 or 98 cents, cover the redemptions, and move on. You don’t permanently shut the door on a building full of healthy assets. Unless the buyers are offering something closer to 80. Or 70. Or lower. Then you shut the door. BlackRock held a company in their fund called Infinite Commerce. One quarter, it was marked at 100 cents on the dollar. The next quarter, zero. Not 80. Not 50. Not 20. Zero. No step down. No gradual repricing. They just moved the slider to total loss. And this brings us back to that Rubric Capital quarterly investor letter. A hedge fund founded by a former portfolio manager at Point72, one of the most respected quant firms on Wall Street. Their words: “Our key takeaway from this behavior is that distribution cuts are so worrisome that some bad actors are playing Enron-like accounting games.” Enron. The most egregious use of accounting fraud in modern-day public company history. A troubling accusation, to say the least. And they’re not the only ones asking questions. The Department of Justice has publicly warned about “creative” marks and divergent valuation practices across private credit portfolios. When a hedge fund says Enron and the DOJ starts asking about your marks, the problem goes deeper than perception. The math is broken. Now let’s talk about where the income is actually coming from. You’d assume that when a private credit fund reports income, that income is cash. Borrowers making interest payments. Checks clearing. Money in the door. Not always. A growing chunk of private credit income is coming from something called PIK, or Payment in Kind. Instead of paying interest in cash, the borrower pays by adding more debt to their loan balance. They owe you $100 million | 1,399 BTC at 10%. They can’t make the $10 million | 140 BTC interest payment. So instead, the balance becomes $110 million | 1,539 BTC. The fund books $10 million | 140 BTC in “income.” But no cash came in the door. The borrower just owes more. And the fund just got a little less liquid. Can you imagine calling your mortgage company and saying, “I can’t make my payments this year, so just add it to the balance. I’ll pay you eventually. Promise!” Right. For publicly traded BDCs (Business Development Companies, which are essentially private credit funds that trade on public stock exchanges), PIK now accounts for about 8% of total investment income on average. At least, that’s the number they have to disclose. For private funds? The ones with no public reporting requirements? Some are running 15 to 20%. No cash, just IOUs stacked on top of IOUs. And here’s the thing about PIK. When a borrower can’t pay interest in cash, the credit has already deteriorated. You’re just not seeing it in the default statistics yet. Because technically, nobody defaulted. They just stopped paying. And remember Cliffwater from Section 2? Three negative months since 2019. Through COVID. Through the fastest rate-hiking cycle in 40 years. Through a regional banking crisis. The S&P 500 had over 20 negative months during that same period. But Cliffwater was absolutely rock solid through the whole period of uncertainty. Three versus twenty. Which leads to the question… Are Cliffwater’s managers among the greatest investors who ever lived, or are the marks wildly optimistic? I know which one I’d bet on. 🛡️ What This Means for Your PortfolioSo where does this leave you? First, find out if you’re exposed. If you have a pension, request the annual report. Look for allocations to “private credit,” “direct lending,” “alternative income,” or “private debt.” If any of those terms appear, some of your retirement is in this market. To be honest, there may be little you can do about it now. But at least you know. And I’ve seen more than one pension impaired by things like this before. If you have a 401(k), check your fund options. Many target-date funds and “alternative” options now include private credit allocations. It won’t say “shadow banking” on the label. Look for “floating rate,” “senior lending,” or “private income.” This one you can actually do something about. If you see private credit exposure in your 401(k), you can reallocate into index funds, bond funds, or money market options. Talk to your plan administrator. If you have a life insurance policy or an annuity, the company backing it is almost certainly a buyer of private credit. You can’t control that. But you should know it. Second, arm yourself with the right questions. Whether it’s your financial advisor, your pension administrator, or your 401(k) provider, here are five questions you should be asking right now: 1. What percentage of my portfolio is allocated to private credit or direct lending? 2. Are any of those funds currently gating or limiting withdrawals? 3. How are the holdings valued? Mark-to-market or mark-to-model? 4. What percentage of the income is PIK (payment in kind) versus actual cash? 5. What is the fund’s current liquidity buffer? Most investors have never asked these questions. Most advisors won’t expect them. Ask them anyway. Third, understand what to watch. More gates mean more problems. Every fund that locks the door increases the pressure on every fund that hasn’t. Investors see one gate and rush to redeem from the next fund before it gates too. We saw this with the regional banks in 2023. One domino tips, and the line gets shorter fast. Watch the quarterly redemption reports. If funds are consistently getting requests above their 5% caps, the mismatch is getting worse, not better. And watch JPMorgan. When the largest bank in America marks down your loans and pulls back on lending, it squeezes the funds from both sides. Their assets are worth less, and their access to capital just got more expensive. For a fund already gating, that combination is suffocating. But here’s what really concerns me. When a fund gates, the investors who needed that cash don’t just shrug and wait. They go find it somewhere else. They start pulling from their other funds. The ones that aren’t gating. The ones that are actually healthy. El-Erian described it perfectly this week, echoing my quote from last week’s newsletter on the sudden need for liquidity: “If you can’t sell what you want, you sell what you can.” That’s the ATM scenario. You needed cash from Fund A, but Fund A locked the door. So you pull from Fund B and Fund C instead. Now those funds are facing redemption pressure they didn’t create. And if enough people do this at the same time, Fund B puts up its own gates. Which sends more people to Fund C. This is how liquidity problems become everyone’s problem. The line between a cash crunch and actual insolvency blurs faster than anyone expects. We watched it happen with First Republic in 2023. That bank was technically solvent. But everyone assumed it wasn’t, and $100 billion | 1,398,895 BTC simply walked out the door. But, here’s the thing. Private credit doesn’t have deposit insurance. There’s no Fed backstop waiting in the wings. When the line starts to blur here, there’s no safety net. And here’s something else worth noting. Right now, there is an executive order worming its way through Washington that would open up 401(k) plans to even more private credit investment. More retail money flowing into the same market that just started locking the gates. Just ask yourself, when’s the last time Congress did anything that was good for you? Again, I’m not telling you to panic. Selling everything and going to cash because you read a newsletter is just a knee-jerk reaction. What you need is a disciplined and coherent strategy. When a $3 trillion | 41,966,846 BTC market starts locking the gates, when the biggest bank in America starts marking down the loans, when a hedge fund with serious institutional pedigree uses the word “Enron” in a letter to investors, you must pay attention. You check your exposure. You ask your fund managers the hard questions. The ones that nobody else is willing or understands enough to ask. You make sure you understand where your money actually is and what it’s actually invested in. Because the one thing every investor who got hurt in 2008 has in common is this: they didn’t look until it was too late. But we’re not going to do that this time around, are we? ─── 👀 What I’m Watching This Week • Cliffwater’s next redemption window. They just capped at 7% on 14% requests. • JPMorgan’s lending posture. Are they tightening further? • Morgan Stanley’s North Haven fund. Capped at 5%. How much was requested? • SEC or Fed commentary. So far, silence. • The Trump 401(k) executive order. Is it still moving forward? ─── That’s it. I hope you feel a little smarter knowing what private credit is, why it matters, and what’s really happening behind the gates right now. If you found value in this, share it with someone you think would benefit. And if you’re not yet a premium subscriber, I’d love to have you join us. Talk soon, James ✌️ As always, I’d love to hear your thoughts. If this article resonates with you or raises questions, please reply and share your perspective. And if you haven’t done so already, I invite you to explore more resources and discussions for dentists navigating the changing monetary landscape at TheBitcoinDentalNetwork.com. Mark R. Link D.D.S. |

The Bitcoin Dental Network

I’m a restorative dentist who got a hard wake-up call during the 2008 financial crisis. Since then, I’ve poured thousands of hours into understanding money, risk, and why costs keep rising in healthcare. I share the most useful, actionable resources I’ve found—especially for dentists, but helpful to anyone—so you can protect your financial health and your practice. That’s why I built The Bitcoin Dental Network. It’s free, practical, and no strings attached.

Hello Reader, All, In my last newsletter, I wrote about why Bitcoin bear markets are often where conviction is built. For those who purchased bitcoin at or near its recent highs, I know that idea may not feel especially comforting right now. Watching the dollar value of an investment decline is painful, and it is completely understandable to wonder whether the original decision was a mistake. I do not want to dismiss that concern or pretend that volatility is easy. But I do want to encourage...

Hello Reader, For those who attended my presentation in Tuscaloosa last August, I know the current bitcoin price action may feel discouraging. Watching bitcoin fall in dollar terms is never fun, especially if you are newer to the asset and still trying to understand whether you made the right decision. But here is the important context: this is not unusual for bitcoin. In fact, it is one of the most normal, recurring patterns in bitcoin’s history. Since bitcoin’s inception, every fourth year...

Hello Reader, With a new Fed Chair expected in 2026, most of the attention will be on who gets the job. But as Tom Bilyeu explains in this week’s video of the week, the more important question is whether the system has any real options left. This is one of the clearest explanations I’ve seen of financial repression, soft default through inflation, and why financial literacy matters now more than ever. I walked you through these principles last August, but this is a much more succinct and...