I’m a restorative dentist who got a hard wake-up call during the 2008 financial crisis. Since then, I’ve poured thousands of hours into understanding money, risk, and why costs keep rising in healthcare. I share the most useful, actionable resources I’ve found—especially for dentists, but helpful to anyone—so you can protect your financial health and your practice. That’s why I built The Bitcoin Dental Network. It’s free, practical, and no strings attached.

Understanding the Financial Waters You’re Swimming In

|

Hello Reader, James Lavish’s latest article gives important perspective on the financial waters all of us are swimming in, whether we realize it or not. Most people assume rising prices are just a fact of life, but over long periods of time, technology should make many things cheaper, not more expensive. The problem is that when value is measured in dollars, exponential debasement hides that reality and pushes people into taking greater risk just to preserve purchasing power. Lavish explains that dynamic clearly, showing why it is hitting younger generations especially hard and increasingly blurring the line between investing and gambling. This article is well worth 20 minutes of your time. 💡 The Casino in Your PocketIssue 113James Lavish, CFAApr 12, 2026∙ Paid ✌️ Welcome to The Informationist, the newsletter that makes you smarter about money in just a few minutes each week. 🙌 One topic. One deep but simple dive. Exposed and explained so you can make better decisions with your money. 🫶 If this was forwarded to you, you have awesome friends. Join 45,000+ readers here. Today’s Bullets:

Inspirational Tweet:

You’ve seen it. Everywhere, all around us. The DraftKings ad before kickoff. The FanDuel promo during the podcast. Your Uber driver checking a Final Four parlay at a stoplight. Your buddy on Kalshi betting on the number of views of a MrBeast video. Betting used to be something you only did in Vegas or Atlantic City. Maybe at the gas station, scratching a ticket while the guy behind you waited for a pack of Marlboros. Now betting is on your laptop, or worse…your phone, in your pocket, all day long. And it happened so fast. Like quicker than a tax hike in California fast. So what’s going on? How did we become a country where betting went from a weekend vacation to an all-day habit? What’s actually driving it? And what does this explosion tell us about the way money works right now? Great questions that deserve serious consideration and answers, ones that we will sift through, nice and easy as always, here today. So pour yourself a big cup of coffee and settle into your favorite seat for a walk through America’s love for wagers with this Sunday’s Informationist. Partner spotThe Downturn Advantage

Bitcoin’s volatility is its advantage. For long-term investors, volatility creates opportunities to build and refine positions over time. Mark Moss recently joined Unchained to explore how bitcoin fits into long-term strategy, and how downturns can be used to position more effectively. The discussion covers:

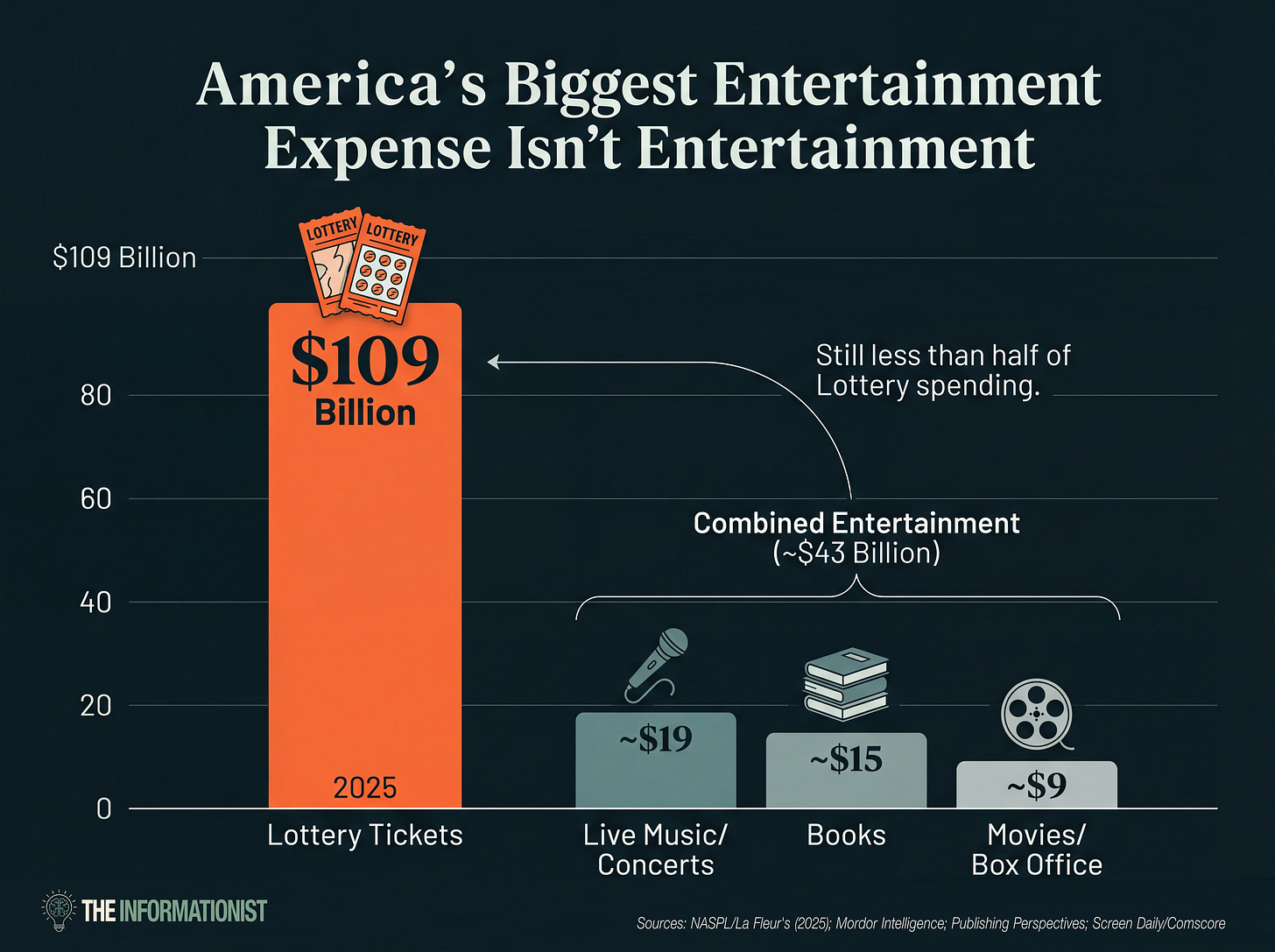

Download the recent collaborative report from Mark Moss and Unchained, Retire Off Bitcoin: The Freedom Investor’s Guide, to access both the report and the full event replay. 🎰 From Scratch-Offs to Super BowlsThe year is 1972, and a nuclear engineer named Mike Kent got bored at work. He was testing reactor designs at a Westinghouse facility in Pennsylvania, feeding punch cards into a mainframe computer. One day, he decided to use that computer to rank the strength of his company’s softball teams. Then he tried it on college football. Then the NFL. He started comparing his computer’s predictions to the odds from local bookmakers. Guys named Primo and Bobo. It worked. He was winning. By 1979, Kent quit his job, stuffed $100,000 | 1.41 BTC cash into a brown paper bag, and drove to Las Vegas. That’s how sports betting worked in America for most of its history. You had to physically go somewhere. You had to carry cash. You had to know a guy. Or a guy who knew a guy. There was friction everywhere, and that friction was the guardrail. The only exception? State lotteries. Governments had quickly figured out that people will pay a voluntary tax if you package it as hope. A $2 | 2,815 sats Powerball ticket. A scratch-off at 7-Eleven. Today, 45 states run lotteries. And look at the result.

Americans spent $109 billion | 1,534,304 BTC on lottery tickets last year alone. More than they spent on concerts, movies, and books combined. Ooof. Still, the lottery was always slow money. Buy a ticket, wait for a drawing, lose, buy another one. The casinos were faster but still required a trip. Vegas. Atlantic City. The tribal gaming halls that popped up across 29 states after the Indian Gaming Regulatory Act of 1988. All of it required you to show up. But all that changed on May 14th, 2018. Because that’s the day the Supreme Court struck down a federal law called PASPA that had banned sports betting in every state except Nevada. The ruling in Murphy v. NCAA told states they could legalize sports betting themselves. That they did. Fast. Sadly, Mike Kent died in a quad bike accident later that same year. The man who started it all with punch cards and a paper bag full of cash never saw what came through that door. Last year, Americans wagered $167 billion | 2,350,722 BTCon sports. Fifteen times what they bet the year the Supreme Court opened the door. And that doesn’t even count prediction markets, zero-day options, or crypto. Something is driving all of this. And it isn’t just big companies or better technology. Oh, it’s something much more troubling. Much worse, in a way. 📱 The ExplosionWe’ll get to the underlying issue. I promise. But first, we need to explore the sheer speed that this all happened. Because the speed tells us something important. An industry doesn’t grow 15x in six years just because the technology got better. That kind of growth comes from demand. Real, urgent, what appears to be desperate demand from millions of people looking for a quick win. Let’s look at the numbers. In 2019, the first full year after the Supreme Court opened the door, Americans wagered $11.3 billion | 159,061 BTC on sports. One year later, $32.8 billion | 461,699 BTC. Then $67.7 billion | 952,957 BTC. By 2024, $149.6 billion | 2,105,797 BTC. And last year? $166.9 billion | 2,349,314 BTC. Fifteen times larger in six years. And still accelerating. The companies saw the demand and flooded it with gasoline. DraftKings pulled in $6 billion | 84,457 BTC in revenue last year. FanDuel controls 44% of the market. Between the two of them, they spent over $2 billion | 28,152 BTC on advertising, plastered across every NFL broadcast, every podcast, every feed you scroll through. Their playbook is simple. Make betting feel as normal as checking the score. Open the app, pick a team, place a parlay, watch the game. Takes less time than ordering Starbucks. And unlike a casino, you never have to look anyone in the eye. No friction. No judgment. Just a few bucks and a phone. Want to place a wager on the doubles semi-final at Wimbledon? No problem. The halftime score of the NCAA Final Four Championship game? Easy. Which team makes the Stanley Cup playoffs? You got it. Eighty percent of all sports bets are now placed on a phone. One in five American adults placed a sports bet last year. In 2018, that number was pretty much zero. Everywhere you turn, it seems like you’re surrounded by people with a horse in the race, any race. Quietly or not so quietly cheering for something.

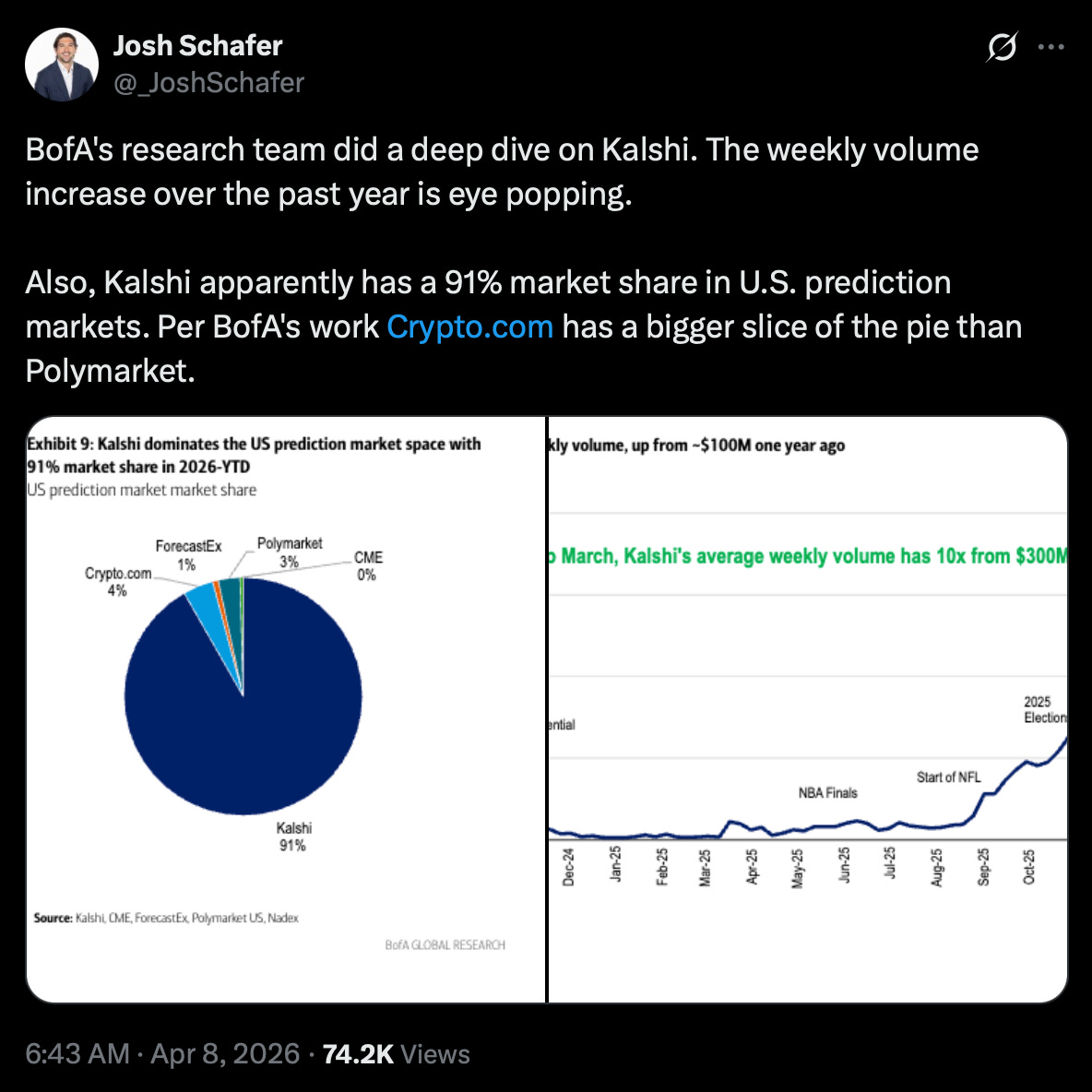

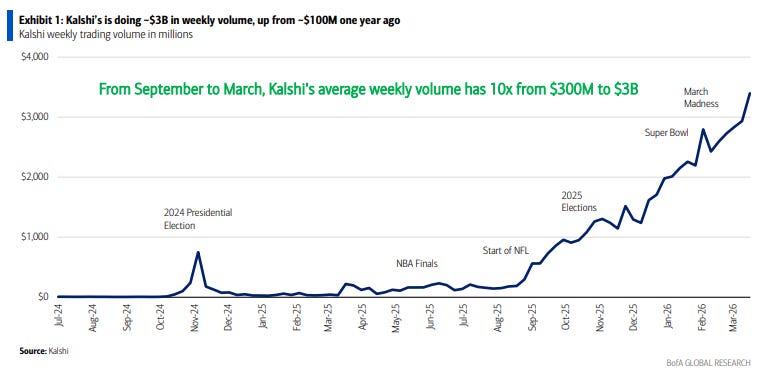

But it still isn’t enough. Prediction markets have taken it even further. Kalshi originally launched as a small, regulated exchange where you could bet on things like economic data releases and weather events. In early 2025, it was doing maybe $100 million | 1,408 BTC a week in volume. In just the first three weeks of March this year, $10.4 billion | 146,392 BTC. With a week left for more. Look at this chart from Bank of America.

What do we see? The 2024 presidential election was a spike that then faded. The real sustained growth started when Kalshi launched sports contracts in January 2025. Then it went vertical and never came back. According to Bank of America, that budding little company called Kalshi now owns 89% of the US prediction market. It has 5.1 million active users, up from 600,000 fifteen months ago. Then in March, Robinhood connected its 27 million brokerage accounts directly to Kalshi’s platform. Think about where we are right now. You can bet on the Fed. On elections. On the weather. On how many views a YouTube video gets. You can do it from the same app where you buy index funds for your retirement account. The infrastructure of betting and the infrastructure of investing have quietly merged. Same apps. Same interfaces. Same clean, professional language. “Event contracts.” “Prediction markets.” On the face of it, it seems insane. And that merger of interfaces raises a philosophical but also consequential question: where exactly does investing end and gambling begin? 🫥 THE LINE THAT DISAPPEAREDGood question indeed. Back when I was working on the floor of the New York Stock Exchange in 1994, there was a story going around about the cheddar cheese futures and nonfat dry milk futures that had just launched on the Coffee, Sugar & Cocoa Exchange. The trading was so thin, so sporadic, that the real action wasn’t in the contracts themselves. It was in the side bets. Traders were wagering more money on when the market would actually open each day than anyone was putting into the futures themselves. It got so bad, the crowds so large, that the exchange threatened to shut the whole thing down. I thought about that story recently. Because that same impulse, the urge to wager on something, anything, in shorter and shorter timeframes, didn’t remain on the fringes of the trading floors. It went mainstream. Because today we have something called called zero-day-to-expiry options. 0DTEs for short. In 2016, 0DTEs represented 5% of all S&P 500 options volume. By 2025, they were 59%. That’s 2.3 million contracts traded every single day. Bets that expire in hours, not months. And who’s trading them? Retail investors. Fifty-one percent of all 0DTE volume comes from individual traders placing short-term directional bets on the index. The mechanics look like investing. You open an account with a broker. You click buttons on a clean interface. You see charts and Greeks and implied volatility. It feels sophisticated. But in reality? You’re betting on whether the S&P 500 goes up or down in the next six hours.

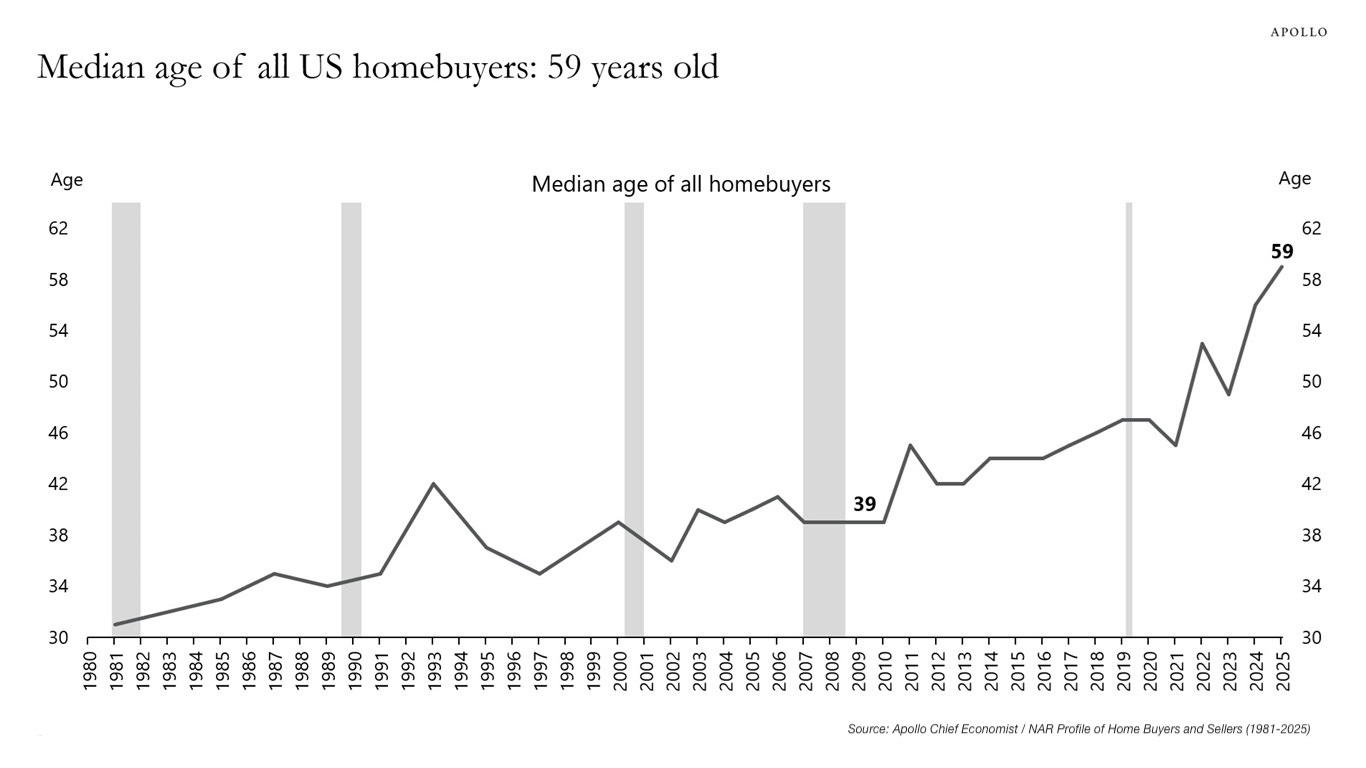

Let’s be honest, that’s not fundamentally different from betting Sunday morning on the outcome of the Masters that very afternoon. The line between investing and betting has all but disappeared. And we need to not make the mistake of thinking that it’s all because of technology making markets more accessible. Because technology didn’t actually change human nature, it just revealed a shift that was already happening underneath. We know this because of a NerdWallet study in 2024 that asked people across generations whether they consider gambling to be a form of investing. Twenty-four percent of Gen Z said yes. Let that sit for a second. It used to be that people accused Wall Street of being a big betting parlor. Now it seems that it’s reversed, and people are saying that Kalshi, Polymarket and DraftKings are actually forms of investing. At this point, you might see where this is all going. See, a different poll last October from Harris Poll canvassed Gen Z and Millennials on the subject of betting. The poll found that 64% of respondents believe that alternative avenues like crypto trading, meme stocks, and sports betting are their only realistic path to building significant wealth. Not patient compounding. Not dollar-cost averaging into index funds. Not meticulously saving for a down payment and buying a home. They think the only way out is to reach for super asymmetric outcomes. Forget compounding at 10% annually in an index fund. That’s too slow, nowhere near lucrative enough. No, they need the big win. The 10x trade that hits overnight. Why? Because the math on the slow path has simply stopped working. Without a big win, they’ll never be able to buy that car. They’ll never own that house. They just can’t catch up. At least not the way the stock market says they’re supposed to. And that brings us to the real question. 💵 The Question Behind All of ItTo understand what is going on here, let’s look at a few pieces of important data first. In 1985, the median home in the United States cost 3.5 times the median household income. By 2025, that ratio hit 5.0x. Homes appreciated 415% since 1985. Household income grew 255%. The gap widened by 160 percentage points. Real wages grew just 18% over 44 years when adjusted for inflation. Less than half a percent per year. But that’s the entire American demographic. Much of that older demographic is doing just fine for reasons that we will get to in a moment. We’re concerned about the lower demographic and the younger generation here. So, what does it look like for them? In short, not good. The median income for a 30-year-old in America is $52,000 | 0.73 BTC. The median home price is $430,000 | 6.05 BTC. Save 10% of your gross income, and the down payment alone takes over 16 years. You’d be 47 before you could walk into a bank with 20% down. By then, the house costs more. Young savers are falling behind faster than ever. And this chart shows the devastating effects of that.

In 1981, the median age of a homebuyer in America was 31. By 2010, it was 39. Today, it’s 59. The typical American buying a home today is closer to retirement than to their first job. The math broke. And they know it. Total household debt in the United States hit $18.8 trillion | 264,632,189 BTC in late 2025. A record. Credit card balances topped $1.28 trillion | 18,017,511 BTC. Thirty million Americans have at least one delinquent account. The system broke the incentive for patience, and people responded exactly the way you’d expect them to. They started gambling. I wrote about this exact structural problem in Issue #200, one of the most-read pieces in the archive. The Cantillon Effect. When central banks print money, it doesn’t spread evenly through the economy. It flows to those closest to the printer first. You can read all about the Cantillon Effect here:

James Lavish, CFA·Jan 11Read full story For you TL;DR types: asset prices rise before wages do. Real estate, stocks, gold and Bitcoin. The people who already own assets get richer. The people trying to save their way into assets fall further behind. Every year, the distance between patience and prosperity gets wider. No surprise, people started reaching. Gamestop. Zero-day options on Amazon or Apple. Prediction markets. Parlays. All the same impulse. A rational response to a system that stopped rewarding the rational strategy. For fifty years, Americans saved less and bet more. And the inflection point lines up almost perfectly with the era of aggressive monetary expansion. The 2008 financial crisis. Quantitative easing. Zero interest rate policy. Trillions in money printing. Savings accounts paid nothing. Bonds paid nothing. The only way to keep up was to take risk. And when the stock market still wasn’t enough, people moved further out on the curve. Options. Futures. Random crypto names. Obscure sporting events. When you break the math on patience, people stop being patient. When the safe path stops delivering, they reach for the dangerous one. That’s what $167 billion | 2,350,722 BTC in sports betting and $10 billion | 140,762 BTC per month in prediction markets tells you. The casino came to America because the alternative stopped working. Understand the incentive structure clearly, and you stop blaming the people chasing 10x bets. Instead you can cast that critical gaze at the system that made patience a losing strategy. More importantly, you start asking better questions about your own money. Where are you on the Cantillon spectrum? Are you closer to the printer, or further from it? And what are you doing (and what can you do) to make sure you’re on the right side of that equation? That’s the real edge. Not a parlay. Not a 0DTE. Not a prediction market. Knowing why the casino exists in the first place. 👀 What I’m Watching This WeekBank earnings. Goldman Sachs reports Monday. JPMorgan Tuesday. Bank of America Wednesday. Deal activity has been surging, and investment banking fees are expected to be up sharply year-over-year. Watch the commentary on consumer credit quality and loan delinquencies. After everything we just talked about, you’ll hear the subtext differently now. FOMC countdown. The next Fed meeting is April 28-29. Futures markets are pricing in a hold. But Thursday’s CPI came in hot (0.9% monthly, driven by energy), and core was softer than expected. That split puts the Fed in an uncomfortable spot. They can’t cut because headline inflation is running. But the underlying economy may not be as strong as the top-line number suggests. Watch for any shift in tone from committee members. But be careful with the knee-jerk read. Dovish signals could actually push long-term rates higher if markets interpret it as tolerance for inflation. The direction depends entirely on the why behind the shift. Iran and oil. Of course, everyone’s watching the weekend developments. Here’s what I’m watching specifically: Brent crude is up roughly 40% since hostilities began. If talks fail, $125 | 175,952 sats+ oil is on the table. That feeds directly into CPI, which keeps the Fed pinned, which keeps mortgage rates elevated, which pushes homeownership further out of reach for the exact demographic we just talked about. The cycle reinforces itself. That’s it for today. I hope you feel a little smarter about what’s really behind the gambling explosion. And the next time you see a DraftKings ad, think about Cantillon. If you found value in this, share it with someone you think would benefit. And if you’re not yet a premium subscriber, I’d love to have you join us. Talk soon, James ✌️ Thanks for reading, and as always, I’d love your feedback. If this article connects with something you’ve been noticing in your own life or practice, hit reply and share your thoughts. For more curated content created to help dentists better understand money, Bitcoin, and the system we’re all working within, visit TheBitcoinDentalNetwork.com. With Appreciation, Mark R. Link D.D.S. |

The Bitcoin Dental Network

I’m a restorative dentist who got a hard wake-up call during the 2008 financial crisis. Since then, I’ve poured thousands of hours into understanding money, risk, and why costs keep rising in healthcare. I share the most useful, actionable resources I’ve found—especially for dentists, but helpful to anyone—so you can protect your financial health and your practice. That’s why I built The Bitcoin Dental Network. It’s free, practical, and no strings attached.

Hello Reader, All, In my last newsletter, I wrote about why Bitcoin bear markets are often where conviction is built. For those who purchased bitcoin at or near its recent highs, I know that idea may not feel especially comforting right now. Watching the dollar value of an investment decline is painful, and it is completely understandable to wonder whether the original decision was a mistake. I do not want to dismiss that concern or pretend that volatility is easy. But I do want to encourage...

Hello Reader, For those who attended my presentation in Tuscaloosa last August, I know the current bitcoin price action may feel discouraging. Watching bitcoin fall in dollar terms is never fun, especially if you are newer to the asset and still trying to understand whether you made the right decision. But here is the important context: this is not unusual for bitcoin. In fact, it is one of the most normal, recurring patterns in bitcoin’s history. Since bitcoin’s inception, every fourth year...

Hello Reader, With a new Fed Chair expected in 2026, most of the attention will be on who gets the job. But as Tom Bilyeu explains in this week’s video of the week, the more important question is whether the system has any real options left. This is one of the clearest explanations I’ve seen of financial repression, soft default through inflation, and why financial literacy matters now more than ever. I walked you through these principles last August, but this is a much more succinct and...